You know that moment when you think buying a building sounds simple, and then the lender starts asking about debt service coverage ratio, lease rollover, sponsor liquidity, and your “global cash flow” like you’re applying to join a secret club? Yes. That one.

Commercial real estate loans are where beginner optimism goes to learn some manners. The good news is that the rules are not random. The annoying news is that they are not consumer-mortgage rules either, and a lot of first-timers find that out after they’ve already fallen in love with a property.

If you are trying to buy an office, retail strip, warehouse, multifamily building, or mixed-use property in the U.S., you do not need a finance degree. You do need to understand what lenders care about, what kinds of loans exist, and why “approved” is less about your mood and more about the property’s numbers. Which is rude, honestly, but also useful.

The Thing Nobody Actually Says Out Loud

The first thing beginners miss is this: commercial real estate loans are not really about the building alone. They are about the building, the borrower, the income, the exit plan, and the lender’s comfort with all four. A house loan is mostly “can you pay this?” A commercial loan is “can this property pay for itself if your life gets weird?”

That is the part people skip because it sounds less glamorous than “I bought my first investment property.” But it matters more than the shiny part. Lenders are not impressed by your confidence, your Canva deck, or the fact that the roof “looks fine from the street.” They want numbers that survive stress.

A commercial loan is basically a bet on the property’s cash flow, not your vibes.

That sounds harsh until you realize it actually protects you too. If the rent roll is weak, the lender should be nervous. If the vacancy is high, they should ask questions. If the tenant base is one guy and a handshake, the approval process should feel annoying. That annoyance is information.

This is why beginners get surprised by the down payment. In the U.S., commercial deals often require roughly 20% to 35% down, and sometimes more depending on the property type, lender, and risk. That is very different from the way people talk about residential loans, where the down payment conversation can feel almost decorative. Here it is not decorative. It is the whole outfit.

Another thing nobody says plainly: commercial lenders love stability more than potential. A small retail center with long-term tenants and boring rent growth may be easier to finance than a cool “value-add” project with upside stories and unfinished plumbing. The bank would rather fund the dull thing that gets paid on time than the exciting thing that needs a hero.

That is why beginners often choose the wrong deal first. They buy the property they understand emotionally, not the one the lender understands financially. And lenders are the audience that matters on day one. It’s a little insulting, yes. Also accurate.

If you want a real-world comparison, think of it like renting a car versus buying one for a road trip. A personal loan is the rental desk asking if you have a license and a card. A commercial loan is the fleet manager asking where you’re driving, how many miles the car will take, who else will use it, and whether you can cover damage if the trip goes sideways. Same vehicle. Much less charm.

The good news is that commercial lending is learnable. Once you see the logic, the process stops feeling mystical and starts feeling like a checklist with a strong opinion. That opinion is usually: show me income, show me equity, show me experience, and do not make me guess how you plan to repay me.

How This Actually Works — The Real Mechanics

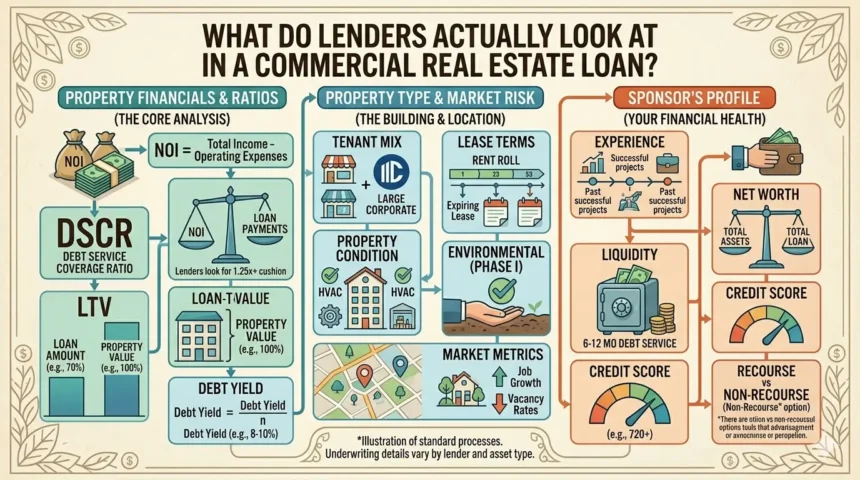

A commercial real estate loan usually starts with the property’s projected income. The lender looks at rent, operating expenses, vacancy, and debt service to see whether the building can support the loan. The key ratio is often the debt service coverage ratio, or DSCR, which compares net operating income to annual loan payments. In plain English: if the property earns enough to comfortably cover the debt, the lender relaxes a little.

Here is the niche corner beginners miss: lenders do not just underwrite the rent. They underwrite the quality of the rent. A six-unit apartment building with scattered lease expirations can look very different from a fully leased warehouse with one major tenant and a ten-year lease. Same “income,” very different risk.

Most beginners also do not realize that commercial lenders often care about the borrower as a sponsor, not just a person. That means your net worth, liquid cash, experience with similar properties, and sometimes your other real estate holdings all matter. If you have never owned commercial property before, that does not kill the deal. It just means the lender may want more cash, stronger reserves, or a more seasoned partner.

A few mechanics matter every time:

- LTV, or loan-to-value, usually limits how much the lender will finance. Lower risk properties can get better leverage, but lenders still like a cushion. They are not trying to be your most enthusiastic backer.

- DSCR tells the lender whether the income can service the debt. If the ratio is too thin, expect problems. Banks do not enjoy “thin.”

- Amortization controls the pace of repayment. A longer amortization lowers monthly payments, but many commercial loans still have shorter actual terms than the repayment schedule. Yes, that little trick has annoyed borrowers for decades.

- Personal guarantee means you may be personally on the hook if the deal fails. Beginners often assume the building is the only collateral. It rarely ends there.

- Reserves are cash set aside for repairs, vacancies, or payment disruptions. Smart lenders like reserves because buildings, unlike spreadsheets, do break.

- Prepayment penalty can make early refinancing expensive. People ignore this until the market changes and they want out. Then they read the fine print like it insulted their family.

The part generic articles miss is how much the property type changes the whole conversation. Multifamily is usually easier to finance than specialty property because the income is more legible. Warehouses can be attractive because leases are often cleaner and tenants simpler. Retail can be fine, but tenant quality matters a lot more than beginners expect. Office has become a trickier category because lenders remember that empty square footage is not a business plan.

And yes, the building’s location matters, but not in the vague “location, location, location” way people say when they have run out of actual thoughts. It matters in a lender’s language: market liquidity, tenant demand, replacement cost, and exit options. A good property in a market with thin buyer demand can still get tougher terms. Lenders want to know how easily they can get their money back if they ever need to.

Comparison — What’s Actually Different Between Your Options

| Option | What it actually does | Who it’s for | The catch |

| Conventional commercial loan | Funds a property based on income, borrower strength, and collateral | Buyers with decent credit, stable income, and some experience | Usually stricter underwriting, more documentation, and larger down payments |

| SBA 504 loan | Helps finance owner-occupied business real estate with lower down payment needs | Business owners buying space for their own company | Rules are specific, timing is slower, and the property must fit SBA use tests |

| SBA 7(a) loan | Flexible financing for business use, sometimes including real estate | Small business owners who need broader financing | Can be more expensive and less clean for pure real estate deals |

| Bridge loan | Short-term funding to buy, fix, or stabilize a property | Investors who need speed or a temporary solution | Higher rates and a refinance deadline staring at you the whole time |

| DSCR loan | Focuses heavily on property cash flow rather than personal income | Investors with strong rental income and less traditional W-2 profiles | Easier in some ways, but the property still has to perform |

My take: if you are a true beginner buying your first commercial property, the best route is usually the one that matches the property type and your actual experience, not the one that sounds coolest on a podcast. SBA loans can be excellent for owner-users. Conventional is often the cleanest for stabilized income properties. Bridge loans are for when you need speed and can handle pressure without acting surprised by it.

What Actually Happens When You Try This

The first thing that hits you is how much paperwork shows up. Not “send us a W-2 and a pay stub” paperwork. More like tax returns, rent rolls, operating statements, entity docs, bank statements, property insurance details, borrower financials, and sometimes explanations for deposits that looked normal to you but suspicious to an underwriter. Everyone thinks the hard part is getting approved. The hard part is gathering the proof in a shape the lender accepts.

What surprised me most in commercial lending conversations is how often the lender keeps coming back to the same quiet question: “If this deal goes wrong, how messy is it?” That one question sits behind the LTV, the DSCR, the reserves, the guarantees, and the appraiser’s assumptions. The surface details change. The fear does not.

Beginners also underestimate the lender’s attention to the lease file. In multifamily, you may get away with a simple rent roll and normal occupancy. In office or retail, one weak tenant can change the whole mood of the deal. A property with good headline rent but a pile of short-term leases can feel stable right up until you look closely. Then it turns into a calendar problem.

There is also a pattern almost nobody writes about clearly: the best-looking properties are not always the easiest to finance. A pristine but expensive building may get tougher terms if the price stretches the lender’s comfort zone. A slightly older property with strong cash flow, boring tenants, and a rational price can look far better on paper. Lenders like boring when boring pays.

If you have never been through it, the appraisal can feel like the least emotional step, which is exactly why it can still sting. The appraiser is not there to validate what you want to believe. They are there to give a market opinion, and that opinion can blow up a cute little spreadsheet fantasy very quickly. A surprising number of deals die here, quietly, which is very on-brand for finance.

The first-time borrower who does well usually does one thing differently: they stop asking, “How much can I borrow?” and start asking, “What kind of deal can I finance cleanly?” That shift changes the whole process. It makes the lender less mysterious and the property more readable.

The Advice Everyone Gives vs What Actually Works

People love saying, “Just get pre-approved.” Fine. But commercial pre-approval is not magic, and it is not a promise. It usually means a lender has reviewed some of your financials and thinks you may fit a certain box, not that every property in the box is okay. The better move is to get pre-qualified for a property type and deal size, then find a building that fits that exact lane.

Another common line is, “Shop around for the lowest rate.” That advice is incomplete because the lowest rate can hide the worst terms. A slightly higher rate with better prepayment flexibility, lower fees, and a sane amortization can be a better deal. Beginners often chase the headline number and then pay for it in fees, covenants, or refinance pain later.

People also say, “Just put more down and you’ll be fine.” Sometimes that helps. Sometimes it only proves you have more money to lose on a weak asset. A bigger down payment does not fix a bad lease structure, a shrinking market, or a property with ugly deferred maintenance. Cash solves some problems. It does not turn a bad building into a good one.

Then there is the classic: “Get the deal under contract first, then figure out financing.” That is how people end up frantic, underprepared, and weirdly offended by lender questions. The realistic move is the opposite. Build your financing profile first, then shop for properties that fit the terms you can actually get. That sounds less dramatic because it is. It also works better.

My actual opinion is that beginners should care less about impressing lenders and more about removing reasons for a lender to say no. Clean financials, stable income, reasonable leverage, and realistic reserves beat cleverness almost every time. Commercial lending rewards not looking like a problem.

The Practical Part — What To Actually Do

Start by deciding what kind of property you want to buy and whether you plan to occupy it. Owner-occupied deals can open the door to SBA financing, while pure investment properties usually follow different rules. This one decision changes the whole lending path, so do not leave it vague.

Pull together your financial package before you talk seriously to lenders. That should include personal tax returns, business tax returns if relevant, bank statements, a personal financial statement, and a rough list of assets and debts. If your numbers are messy, clean them up now, not after a lender asks why a deposit looks strange.

Study the property’s income like a lender would. Look at rent roll, occupancy, lease expirations, operating expenses, and any obvious repair issues. If you cannot explain why the building should support the debt, a lender is not going to pretend for you.

Ask directly about the down payment, DSCR requirement, reserves, prepayment penalty, and whether a personal guarantee is needed. Those are not side questions. They are the deal. If a lender dodges them early, that is not mystery. That is information.

Compare at least three financing options before you choose one. A conventional loan, an SBA route, and a bridge or DSCR option can look very different once you factor in fees and flexibility. The cheapest rate is not always the cheapest loan, which is the kind of sentence that should be printed on a mug and handed to every first-time buyer.

Get realistic about your own experience level. If this is your first commercial deal, a partner with experience can help more than a slightly better rate. Lenders trust a clean team, and so should you.

Finally, leave yourself more cash than the bare minimum. Repairs happen, vacancy happens, and closing costs happen in a way that always feels more expensive than the spreadsheet suggested. People hate hearing that. The market does not care.

So Where Does This Leave You

If you are a beginner, the honest answer is that commercial real estate loans are not impossible. They are just less forgiving than people expect. That is not a reason to quit. It is a reason to stop guessing.

The useful move today is simple: pick one property type, write down the likely loan type, and list the four numbers a lender will care about most — down payment, DSCR, reserves, and monthly debt payment. Once those are in front of you, the whole thing becomes less dramatic and more manageable. Not easy. Just manageable.

The people who do well here usually are not the loudest ones in the room. They are the ones who brought paperwork, cash, patience, and a healthy suspicion of “easy” deals. Which, frankly, is a very respectable way to buy a building.

If you can get those basics right, you are already ahead of a lot of first-timers who are still waiting for the lender to be magical.

Conclusion

You made it through the part where commercial real estate stops being a cool phrase and starts looking like a stack of documents with opinions. Respect.

The real lesson is pretty simple: the loan follows the deal, not the dream. If the numbers work and the property makes sense, you have a shot. If they do not, the lender will help you discover that the hard way, which is not personal, just expensive.

So start with the property, not the fantasy. Finance rewards the boring parts more than anyone admits.