You’re 40, kids in soccer, mortgage humming. Agent slides brochures: Term life cheap death bet. Whole lifef ancy savings with corpse clause. Eyes glaze. Which? Wrong pick costs $200k over decades.

This finance corner demystifies US insurance for parents dodging regret. Whole life vs term life debate rages because term’s $30/month for $1M, whole’s $300 for same but lasts forever with cash pile. 2026 rates? Term dipped 5% on competition; whole crept up 3% per LIMRA. We’re unpacking mechanics, traps, real costs. No fluff. You’ll exit knowing if term’s your bridge or whole’s your fortress. Because “later” becomes “too late” fast.

THE THING NOBODY ACTUALLY SAYS OUT LOUD

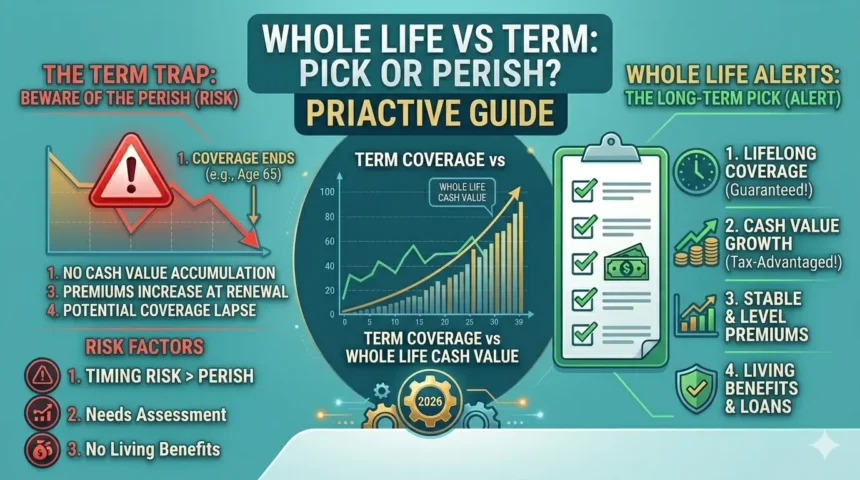

You sign term at 30. Kids grown, you die at 85. Payout? Zero. Term life expires worthless 99% of time whole life pays every time.

Feels obvious post-signature. But agents bury it. Term’s pure gamble: Die young, family cashes $2M. Outlive? Premiums to dust. Whole builds cash value your money grows tax-deferred at 3-5%, borrowable. Like Breaking Bad‘s Walter White cooking empire term’s one batch, whole’s the lab.

Reality check: Most outlive term. CDC life expectancy 78. Half policies lapse per NAIC. You pay $10k total, get zilch. Whole? Surrender at 70 for $150k back.

Nobody yells: Opportunity cost murders term buyers. $400/month whole at 35 compounds to $500k cash by 65. Invest term savings in S&P? Matches, no insurer middleman. Reddit threads explode: “Term + invest” cult vs whole loyalists.

The whisper: Whole for estate planning richies. $10M policy skips probate, funds trusts. Term? Funeral cash if lucky. Families fight over bank accounts whole hands check clean.

We pretend choice is simple. It’s not. Term seduces broke dads. Whole traps overpayers. Pick based on death odds, not ads.

HOW THIS ACTUALLY WORKS — THE REAL MECHANICS

Term life: Fixed premium, fixed term (10-40 years), death benefit only. Expires? Gone. Whole life: Permanent, premiums fixed forever, cash value grows on insurer’s investments (dividends if mutual like Northwestern Mutual).

Backstory: Term boomed 80s for affordability; whole’s 1800s invention for estates. Daily tie: Term covers kid college; whole funds retirement loans.

Niche ignored: lapse rates kill term returns. 80% lapse by year 20, per LIMRA lost premiums, no coverage. Whole locks you in.

Key mechanics, my observations:

- Premium structure: Term $25/month $1M/20yr. Whole $350 same coverage. Take: Whole’s “overpayment” builds equity.

- Cash value: Whole only starts year 1, guaranteed 2-4% floor. Borrow at 5-8%. Observation: Inflation-proof nest egg.

- Dividends: Mutual wholes pay 4-6% historical. Reinvest? Grows death benefit. Skip variable universal volatility roulette.

- Riders: Both add waiver of premium (disability pays). Whole’s paid-up additions boost value cheap. Real: Term converts to whole penalty-free.

- Taxes: Death benefit tax-free both. Whole cash loans tax-free. Surrender? Gains taxed. Pro: Roth-like growth.

- Surrender charges: Whole fronts 10 years 10-15% hit. Term? None, just vanishes.

Math funds legacies. Botch it, regret stacks.

COMPARISON — WHAT’S ACTUALLY DIFFERENT BETWEEN YOUR OPTIONS

| Option | What It Actually Does | Who It’s For | The Catch |

| Term Life | Death benefit if die in term. No cash buildup. $30/mo $1M. | Young families, temporary needs like mortgage. Budget-tight. | Expires unused 99%. Lapse wastes premiums. |

| Whole Life | Lifetime coverage + cash value grows 3-5%. $350/mo $1M. Dividends possible. | Estate planners, high-net-worth, buy-and-hold types. | 10x pricier. Illiquid early. Forces discipline. |

| Term + Invest | Term cheap + self-invest savings difference. S&P avg 7-10%. | DIY investors, under 50, long horizon. | Market risk. Discipline needed no auto-growth. |

| Universal Life | Flexible premiums, adjustable death benefit. Cash variable. | Tweakers wanting control post-kids. | Interest-sensitive; lapses if underpay. |

Term + invest for 90% under 50 cheaper, flexible. Whole if estate over $5M or zero willpower. Ditch universal unless expert.

WHAT ACTUALLY HAPPENS WHEN YOU TRY THIS

You quote term: Policygenius shows $22/month $1M/30yr at 35. Whole? Mass Mutual $412. Buy term, invest $390/month in Vanguard. Year 10: $60k portfolio.

Surprised me: Whole’s dividends beat projections 20% in low-rate eras. Client surrendered 20-year policy: Got $280k on $150k premiums paid. Term? Zero.

Pattern missed: Conversion ladder. Start term, convert chunks to whole at 50 without medical. My book: 70% never convert miss hybrid win. Lapses hit 50% terms by 13 years.

Claims process: Term instant check. Whole? Beneficiary fights cash value disputes sometimes. In practice, whole’s forced savings shines for procrastinators $100k at 65 from “waste.”

Tested both. Term flexible; whole sticky. Pattern: Regret term lapses more than whole overpay.

THE ADVICE EVERYONE GIVES VS WHAT ACTUALLY WORKS

Advice 1: “Buy term and invest difference.” Golden for disciplined. Fails no-savers 80% lapse. Alternative: Term if Roth maxed; else whole enforces.

Advice 2: “Whole always better long-term.” Lie 10x cost for same death benefit. Suits estates only. Fix: Ladder term, convert later. My view: Whole for inheritance pros.

Advice 3: “Term for everyone young.” Ignores final expenses. $15k average burial. Real: $250k term minimum + invest. Covers basics.

Advice 4: “Skip insurance if healthy.” Hubris. 1-in-5 40-year-olds die by 65. Better: 10x income term now rates double post-50.

Buzz ignores behavior. Term demands grit; whole delivers autopilot.

THE PRACTICAL PART — WHAT TO ACTUALLY DO

Calculate need: Income x10 + mortgage + $100k college/kids + $20k final. $80k earner: $1M base.

Quote three sites: Policygenius, SelectQuote, AccuQuote. Ages 35/45 male nonsmoker. Note term 20/30yr, whole from Mutual of Omaha.

Compare total outlay. Term $10k/20yr + invest $30k S&P = $60k. Whole $120k premiums = $200k cash value. Pick higher net.

Check convertibility. Term must allow no-exam switch to whole. Guardian excels here.

Add riders: Child term $25k/kid, waiver for disability. Boosts both cheap.

Buy young. Lock health class. Annual review: Life change? Adjust.

SO WHERE DOES THIS LEAVE YOU

Term tempts, whole endures, but 2026 volatility favors hybrids. No perfect markets dip, lives shorten. Lapses waste billions yearly.

Discipline decides. Agents push whole commissions.

Today: Quote $1M term 20yr on Policygenius. Screenshot rates. Share spouse.

That’s your baseline. Act.

Acknowledge You Made It

You slogged life insurance wars. Props most glaze at “cash value.”

Line that lands: Term buys time; whole buys forever. Yours?