You know that feeling when a credit card ad sounds almost suspiciously polite? Zero interest, no annual fee, maybe even a bonus on top. Nice little deal, until you notice the part where the fine print has quietly arranged itself into a small legal ambush.

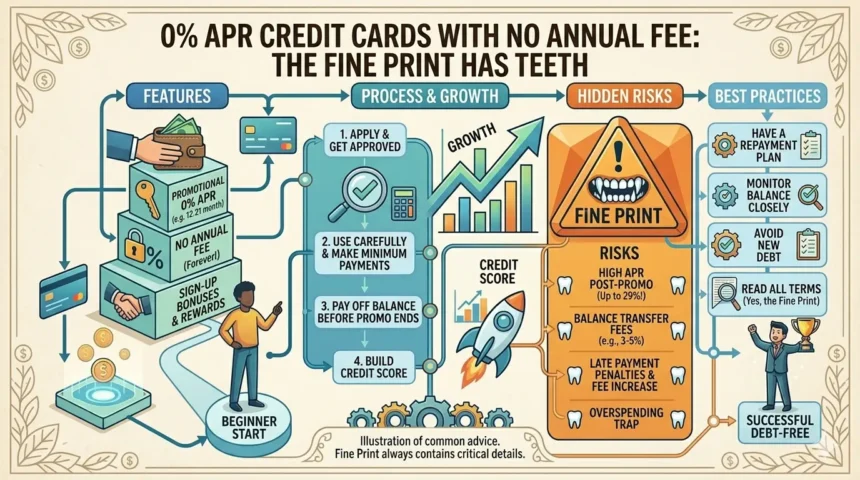

That is the whole story here. People search for 0% APR credit cards with no annual fee because they want breathing room, and they are not wrong to want it. The trick is that these cards are useful in two very different ways: some help you finance a purchase without interest, and some help you move debt around without lighting extra money on fire. The same card can be a smart move or a very expensive confidence trick, depending on how you use it.

The good news is that the category is real, common, and often worth using. The less glamorous truth is that you only win if you understand the clock, the fees, and your own habits. Cards like the Wells Fargo Reflect, Citi Simplicity, BankAmericard, and Capital One VentureOne all show the basic shape of this market in 2026: no annual fee, a temporary 0% APR offer, and a regular APR waiting patiently in the wings. That patience is the whole problem.

The Thing Nobody Actually Says Out Loud

The best 0% APR card is not the one with the flashiest intro period. It is the one you can survive after the intro period ends.

That sounds less exciting than an ad campaign, but it is the part people skip. A 21-month offer sounds long because it is long, yet long is not the same as harmless. If you put $3,000 on a card, then pay it like a person who “mostly remembers” due dates, the promo period can still end before the balance does. Then the regular APR shows up, and regular APR is where the card company stops being charming.

There is also a quiet split most articles flatten into one blob. A 0% offer on purchases helps when you are buying something new and want time to pay it off. A 0% offer on balance transfers helps when you already owe money and want to move it somewhere colder. Those are not twins. They are cousins at best, and one of them asks for a transfer fee, which is how the deal pays for itself.

The catch is not the fee. The catch is the deadline.

That deadline changes behavior in a way people underestimate. You stop thinking like a long-term borrower and start thinking like a project manager with a mildly embarrassing spreadsheet. That is not bad, exactly. It is just not how most people enjoy using credit cards.

A lot of the appeal is psychological, which is why these cards show up in January, after vacations, after car repairs, and after someone says, “I’ll just pay it off next month.” That sentence has paid for several vacations, a dishwasher, and probably one regrettable wedding registry item. The card is useful because life is messy. The card is dangerous because life stays messy longer than the promo period.

How This Actually Works — The Real Mechanics

A 0% APR offer usually lasts a fixed number of billing cycles, not forever. Credit Karma’s 2026 listings show examples ranging from 12 months to 21 months, including Wells Fargo Reflect at 21 months on purchases and Citi Simplicity at 18 months on purchases and balance transfers. The number that matters is not just the length of the intro period. It is whether the offer applies to purchases, balance transfers, or both.

Balance transfers are where people get a little too poetic. They imagine debt vanishing. It does not vanish. It moves. Usually you pay a transfer fee, often around 3% to 5%, and the new card may require transfers within a set window after opening the account. So yes, you may be saving on interest. No, you are not getting free money. Credit card companies are many things. Generous is not usually one of them.

Here is the corner most generic articles miss: these cards are really time-management tools. They reward people who can set up payments, track due dates, and avoid adding new debt while the old debt is still sitting there. That is why the best fit is often someone with one specific goal, not someone who just wants “a good card.”

- Purchase-focused cards are best when you have a planned expense, because you can spread it out without interest if you actually finish the job on time.

- Balance transfer cards are best when your current APR is ugly, because moving debt to 0% can cut the damage fast.

- Cards with rewards can be a decent bonus, but only if the rewards do not distract you from the payoff plan.

- Long intro periods matter more than headline rewards when the balance is large, because time beats points in most real situations.

- No annual fee matters because it keeps the card cheap to park in your wallet after the promo ends, assuming the regular APR does not tempt you into nonsense.

The other real-world detail is this: issuers still underwrite these cards like any other credit product. Good credit usually helps, and the best offers often sit in the “good to excellent” lane. That is why articles about these cards often pretend selection is simple, when in practice it is half math and half whether your credit profile makes the approval process cooperative.

Comparison — What’s Actually Different

| Option | What it actually does | Who it’s for | The catch |

| Wells Fargo Reflect | 0% intro APR for 21 months on purchases, $0 annual fee | People who need a long runway to pay off a purchase | It is only helpful if you can clear the balance before the promo ends |

| Citi Simplicity | 0% intro APR for 18 months on purchases and balance transfers, $0 annual fee | Debt consolidators who want a long window and low fuss | Balance transfer fee applies, and the transfer must happen on time |

| BankAmericard | 0% intro APR for 21 billing cycles on purchases and transfers, $0 annual fee | People who want a balance transfer plus a long purchase window | Transfer fee still exists, so the math matters |

If your goal is the longest runway, Wells Fargo Reflect and BankAmericard are the obvious names in this snapshot. If you want a card that can do both jobs, Citi Simplicity is more flexible, but you still pay for that flexibility through transfer fees. My take: choose the card around the payoff plan, not the other way around. That is how you keep a “deal” from turning into a hobby.

What Actually Happens When You Try This

The first surprise is how fast the offer becomes boring once the account is open. That is good. The excitement fades, and what remains is the part that matters: a number, a due date, and your own discipline.

Most people expect the pain to be the payment amount. It usually is not. The pain is remembering that new purchases may not be covered by the same logic as the old balance, especially on cards with transfer promos and separate purchase terms. That split catches people who think “0% APR” means “everything is free for a while.” It does not. That misunderstanding is responsible for a lot of avoidable interest.

What nobody warns you about here is the feeling of false relief. You move a balance, the utilization ratio may improve over time, and suddenly you feel financially more together than you are. That is the dangerous part. The card can make you look organized before you actually are organized.

Another pattern: people often succeed more with a simple automatic payment than with a heroic payoff plan. The dramatic spreadsheet with color coding is nice. The automatic transfer from checking is what usually saves you. Human beings are not built to manually remember twelve consecutive months of ideal behavior. Shocking, I know.

There is also a spending trap that shows up after the transfer. Some people free up the old card, then start using both cards, and now they have the original debt plus fresh purchases. That is how a tidy consolidation turns into a small financial reenactment of a kitchen drawer that refuses to close. The card did its job. The user did not.

The Advice Everyone Gives VS What Actually Works

One common piece of advice is “always get the longest 0% APR period.” That sounds correct, and sometimes it is. But it is incomplete because a longer offer with a worse fee or a card you barely qualify for can be less useful than a shorter, cleaner option. The grounded version is simple: pick the longest period only after checking the transfer fee, the regular APR, and whether you can realistically pay it off in time.

Another favorite line is “use the card to pay down debt faster.” Fine. That only works if you stop adding debt at the same time, which is where many people fall apart. A better rule is to move the debt, freeze new spending on the old category, and make the card boring. Boring is underappreciated in finance. It pays.

People also say “rewards cards are better because you earn something back.” Sometimes. But rewards are not a meaningful win if you are carrying a balance and chasing interest relief. The smarter move is to treat rewards as a small extra, not the main event. If the APR savings are doing the real work, the points are just a nice condiment.

Then there is the advice to “just pay it off before the promo ends.” Obviously. The problem is that this advice skips the method. What actually works is dividing the balance by the number of promo months, then setting an automatic payment above that amount if you can manage it. That gives you a target instead of a wish, which is a much more usable thing.

The Practical Part — What To Actually Do

Start by matching the card to the job. If you are financing a purchase, look for a strong 0% purchase APR offer. If you are dealing with old debt, look for balance transfer terms and the transfer fee. The difference sounds basic because it is basic, but plenty of people still pick the wrong tool and then act surprised when it behaves like the wrong tool.

Next, calculate the monthly payoff amount before you apply. If you move $4,800 to a 16-month offer, divide that balance by 16 and add a little extra for safety. If that number feels impossible, the card is not the answer. The math does not care about your intentions.

Set autopay the day the account opens. Not “soon.” Not “after I figure out the statement cycle.” The card only works as a plan if the minimum payment at least happens without drama. Better yet, set a second manual payment for the amount you need to clear the balance by the end of the promo.

Keep the old spending category on pause. If you transferred restaurant debt, stop charging meals to the old card until the transfer is under control. If the new card is for a big purchase, avoid using it for random extras that muddy the payoff plan. Clean habits save money because they reduce decision-making, which is where people usually lose.

Read the transfer window and fee before you click apply. Some cards want transfers completed within a short period after account opening. Miss that window and the terms can change. This is the part where the offer stops being a shiny promise and becomes paperwork with consequences.

Check the regular APR too, even if you plan to pay on time. You are not reading it because you expect to fail. You are reading it because people sometimes do fail, and card issuers are completely uninterested in your apology tour.

Finally, treat the 0% period like a countdown, not a benefit. Put the end date in your calendar. Set reminders a month early. Then set another one two months early, because human memory is famously overconfident.

So Where Does This Leave You

It leaves you with a decent tool, not a miracle. A 0% APR credit card with no annual fee is useful when you already know what job it has to do. If you are hoping it will fix messy spending habits by itself, it will not.

The smart move today is simple: check whether you need a purchase promo or a balance transfer promo, then calculate the monthly payoff amount before you apply. That one step tells you whether the card is actually helpful or just politely dressed up debt.

The nice part is that these cards are often genuinely valuable when used on purpose. The annoying part is that “on purpose” is doing a lot of work here.

You made it this far, which means you probably already suspected the deal was not as simple as the headline. Correct. Credit cards rarely are. They just wear a cleaner shirt than the rest of consumer debt.