How to Refinance a Mortgage With Bad Credit

You already know the vibe. Your credit score is doing a bad impression of a respectable number, your mortgage payment is still due like clockwork, and some article on the internet is telling you to “just compare offers.” Sure. Great. Let me just compare offers from the bank that side-eyed me when I opened the checking account.

If you want to refinance mortgage with bad credit, the real issue is not whether refinancing exists. It’s whether the math works well enough for a lender to take the risk. That is the whole game, and most glossy advice skips right past it. The point is not to sound financially pure. The point is to lower your payment, change your term, or get out of a loan that’s quietly draining you.

And yes, people do refinance with bad credit. Not everyone, not easily, and not always into a better deal. But there are real paths. Some are ugly, some are boring, and some only make sense if you stop chasing the perfect rate and start chasing the least-bad outcome.

The Thing Nobody Actually Says Out Loud

Bad credit makes refinancing harder, but it does not automatically make it impossible.

That’s the sentence people want to bury under cheerful mortgage math. The truth is that lenders do not wake up and think, “Let’s help everyone equally.” They price risk. If your score is low, they want more proof that you can pay. That proof usually comes from equity, income stability, a lower debt load, or a refinance program with looser rules.

This is where people get stuck. They assume the score is the whole story. It isn’t. A borrower with a 580 score, stable income, and 40% equity can look better than someone with a 670 score, shaky work history, and barely any equity. That is why the same advice online feels useless. It treats all credit problems like one giant blob.

Lenders do not reward hope. They reward lower risk.

In practice, that means you are not trying to “win” refinancing. You are trying to make your file boring enough for underwriting. That may mean paying down a credit card, waiting for one account to age, or using a government-backed program that cares less about score and more about loan history. Annoying, yes. Surprising, no.

The other thing people skip is this: sometimes refinancing with bad credit only helps if you are fixing one narrow problem. Maybe your current rate is horrible. Maybe your adjustable-rate mortgage is about to reset. Maybe you need to remove mortgage insurance or shorten the term. If your new loan barely improves anything after closing costs, then refinancing is just expensive theater.

Think about it like trying to get into a club wearing the wrong shoes. You can still get in, but the door person is checking everything else harder. Credit score matters. So do income, equity, and payment history. One weak spot can be offset by strength elsewhere. That is the part most people miss, and it is the reason some borrowers get approved while others with similar scores do not.

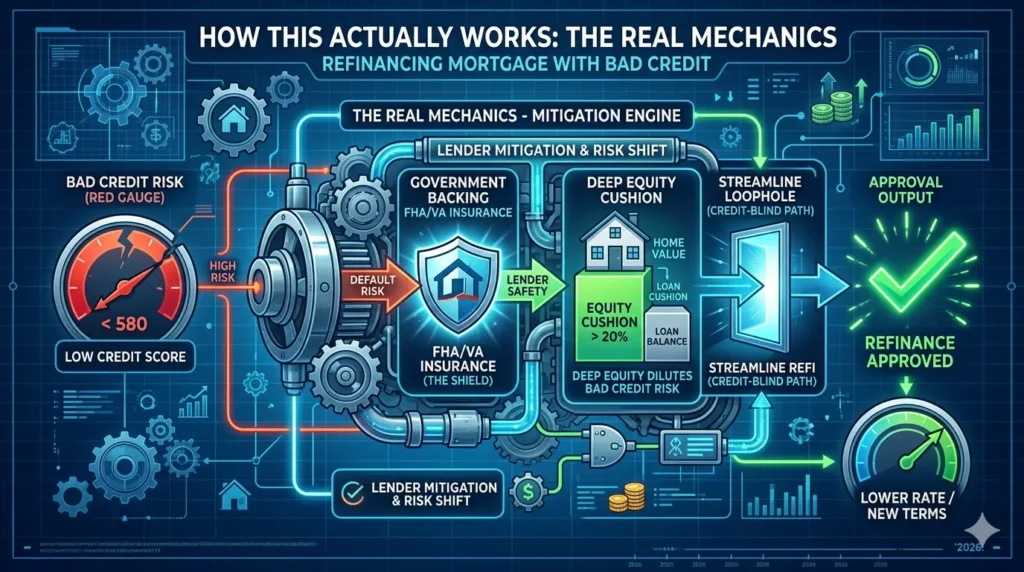

How This Actually Works The Real Mechanics

Refinancing is not one thing. It is a set of loan types with different rules, and that is where the useful part starts. If your credit is bad, the lender is asking two questions: can you pay, and how much skin do you already have in the house? That second question matters more than people think.

Mortgage lenders usually look at your credit score, debt-to-income ratio, loan-to-value ratio, income stability, and payment history. A low score can be offset by strong equity or a clean record on the current mortgage. If you have already made 12 to 24 on-time mortgage payments, that helps a lot more than people expect. Mortgage underwriting is weird like that: your current behavior often matters more than old mistakes.

Here’s the corner most generic articles miss: the type of refinance can matter more than your score alone.

- FHA streamline refinance: useful if your current loan is already FHA and you want easier paperwork; the catch is that it usually does not let you pull cash out, and you still need the loan to make sense.

- VA IRRRL: if you have a VA loan, this can be one of the easiest routes; the catch is that you need the right military eligibility and an existing VA mortgage.

- Conventional refinance: this is where bad credit starts to sting the most, because private lenders are fussier and often charge more.

- Cash-out refinance: this sounds tempting when money is tight, but it is usually the least forgiving option because the lender now sees more risk and you are borrowing more against your home.

- Non-QM refinance: non-qualified mortgage lenders are sometimes more flexible, which helps borrowers with unusual income or weaker credit; the catch is that the pricing can be ugly.

A lot of borrowers make one mistake here: they chase the rate first and ignore fees. That is backwards. If you are paying closing costs and getting a rate that barely improves your monthly payment, you may spend months recouping what you spent to refinance. That can still be fine if you are escaping an adjustable rate or cleaning up a bad loan structure, but it is not magic.

The hidden factor is how close you are to the edge. A borrower at 620 is often treated very differently from one at 580, even if both call themselves “bad credit.” That gap changes your options. So does whether your mortgage is late, current, or recently delinquent. Once a payment has gone late, your choices narrow fast. Mortgage lenders love a clean payment history almost as much as they love low risk.

Comparison What’s Actually Different Between Your Options

| Option | What it actually does | Who it’s for | The catch |

| FHA streamline refinance | Replaces an FHA loan with simpler underwriting | FHA borrowers with a decent payment history | Usually no cash-out, and the loan still has to improve your position |

| VA IRRRL | Refines a VA loan with lighter paperwork | Eligible VA borrowers | Only works if you already have a VA loan |

| Conventional refinance | Replaces your loan with a private-market mortgage | Borrowers with stronger files or more equity | Bad credit usually means higher rates and stricter approval |

| Cash-out refinance | Replaces your loan and lets you borrow extra equity | Borrowers who need cash and have enough home equity | Most expensive path when credit is weak |

| Non-QM refinance | Uses alternative underwriting rules | Self-employed or nontraditional borrowers with credit issues | Flexibility usually comes with worse pricing |

If your current loan is FHA or VA, start there. Those are often the most realistic lanes for borrowers with rough credit. If you are looking at a cash-out refinance just because the monthly budget feels tight, pause first. That route can fix a short-term problem by creating a longer-term one.

What Actually Happens When You Try This

The first thing that surprises people is how much time goes into proving the obvious. You already know you make the payments. The lender still wants pay stubs, bank statements, tax returns, credit explanations, and probably a few follow-up questions that feel suspiciously like a background check for a job you already have.

What people do not expect is how much attention goes to recent behavior. A score from two years ago matters less than a missed payment from two months ago. That single late mortgage payment can change the whole conversation. Same with new debt. If you finance a car, open a bunch of cards, or drain your savings right before applying, the file gets uglier fast.

Here is the pattern other articles miss: borrowers with bad credit often think they need a “better score” before they can do anything. Sometimes what they really need is a cleaner application. Lenders care about the story the file tells. If your score is low because of old medical debt but your mortgage has been paid like clockwork, you may have a real shot. If your score is low because you are currently juggling late payments and maxed-out cards, refinancing gets much harder.

One thing that surprises people is how far a little equity can go. Not enough to erase bad credit, obviously. Enough to make the lender feel less exposed. Homeowners with 20% or more equity often have more room to work with than they expect, even if their score is not pretty. That said, equity is not a costume. You cannot dress up a weak file and pretend it is strong. Lenders see right through that.

I have also seen the same emotional mistake over and over: people apply too early, get denied, and then assume the whole idea is dead. Sometimes the denial is just a signal. Pay down a revolving balance, wait for one late payment to age, or move from “almost current” to fully current. That can change the result more than people want to admit.

The Advice Everyone Gives vs What Actually Works

“Just improve your credit first.” That advice is fine in theory and useless in its simplest form. Yes, better credit helps. But if you need a refinance now because your rate is resetting or your current payment is crushing your budget, waiting six to twelve months may cost more than the refinance saves. The grounded move is to improve the part of your file that changes fastest: pay down revolving balances, fix reporting errors, and avoid new debt while you shop.

“Shop around with every lender.” This is half right. Yes, you should compare lenders. No, you should not shotgun 20 applications just because some blog told you to “let the market compete.” Multiple hard pulls can still matter, and more importantly, not every lender is built for bad-credit borrowers. The real move is to start with lenders that actually do FHA, VA, or non-QM refinances and ask them what minimum files they accept.

“Refinancing only makes sense if the rate is lower.” That is too narrow. A refinance can also remove mortgage insurance in some situations, shorten your term, switch from adjustable to fixed, or stop a nasty loan reset from hitting your monthly budget. I would say this plainly: rate is important, but it is not the only reason to refinance, and sometimes it is not even the biggest reason.

“Wait until your score hits 700.” That sounds tidy and emotionally soothing. It is also unrealistic for a lot of people. If you are sitting on good equity and a harmful loan structure, waiting for a perfect score can be a very expensive act of self-control. Better to ask, “What problem am I solving?” If the answer is cheaper payments or more stability, then the best refinance is the one that fixes that problem without creating a larger one.

The Practical Part What to Actually Do

Start by checking your current loan type and payoff details. You need to know whether you have an FHA, VA, or conventional mortgage, because that changes the menu fast. Then ask for a payoff estimate and compare it with your current rate, balance, and remaining term. People waste time applying before they know what they even have.

Pull your credit reports from all three bureaus and look for errors that are actually worth disputing. A wrong late payment, duplicate collection, or outdated balance can matter more than a tiny score bump from a new app. Do not waste energy fighting everything. Fix the items that directly affect mortgage underwriting.

Figure out your equity position with a realistic home value, not the one you hope to get from a cheerful Zillow page. If you have little equity, some refinance options simply disappear. If you have decent equity, your odds improve even if your score is messy. That is one of the few parts of this process where math is still kind enough to be honest.

Lower your revolving balances before you apply if you can. Credit card utilization has a nasty habit of making a file look worse than it is. Even a few thousand dollars paid down can change how lenders read the whole application. This is one of those boring moves that works because it is boring.

Ask lenders about the exact minimum score, equity, and payment history they want before you submit a full application. The internet loves vague optimism. Lenders do not. Get the actual bar, then compare it to your file. That alone can save you from a denial you could have predicted.

If your current mortgage is FHA or VA, ask specifically about streamline or IRRRL options. These programs exist partly because the system knows not every borrower fits the clean little box conventional lenders like. They are not free passes, but they are often the most realistic path for someone with bruised credit.

Finally, calculate your break-even point. Add closing costs, then divide by the monthly savings. If it takes too long to break even, the refinance may be a bad trade even if you qualify. A cheaper payment is nice. A pointless fee is still a fee.

Can I refinance my mortgage with a 580 credit score?

Yes, sometimes, but your options are narrower. A 580 score can work better with FHA or VA-related routes than with a standard conventional refinance. The stronger your equity and payment history, the better your odds. If the rest of your file is shaky, expect higher pricing or a denial.

What is the lowest credit score to refinance a house?

There is no single number that every lender uses. Some lenders may go lower for FHA-related loans, while conventional lenders often want higher scores. The real answer is that the minimum score changes with the loan type, your equity, and your debt load. That is why “lowest score” is less useful than “lowest score for this specific refinance.”

Can I refinance with bad credit and no equity?

That is a tough one. Without equity, lenders have less protection, so the file has to be strong in other ways. If you have little or no equity, your best shot is usually through a program tied to your current loan type, such as FHA streamline or VA IRRRL, if you qualify. If not, the options get thin quickly.

Is a cash-out refinance possible with bad credit?

Yes, but it is usually harder and more expensive. Cash-out refinance adds risk for the lender because you are borrowing more money against the house. That means stronger equity and better income matter even more. If your credit is already weak, this is often the hardest refinance to get approved.

Does refinancing hurt your credit score?

A refinance can cause a small temporary dip because of the credit check and the new loan account. That is usually not the real issue. What matters more is whether the refinance improves your monthly cash flow and long-term debt position. A tiny score drop is often worth it if the loan itself is better.

How long should I wait after bad credit to refinance?

It depends on what caused the bad credit. A few recent late payments, high card balances, or a new collection can hurt more than an old issue that has already aged. Many lenders want to see a period of clean mortgage payments before they get comfortable. If you are trying to refinance soon, the goal is not “perfect credit.” It is cleaner recent behavior.

Which is easier: FHA streamline refinance or conventional refinance?

FHA streamline refinance is usually easier if you already have an FHA loan and meet the program rules. Conventional refinancing is generally stricter, especially with bad credit. The streamline option exists partly to reduce paperwork and make refinancing more accessible. That is why it is often the better lane for borrowers with bruised credit.

Should I pay for points if I have bad credit?

Usually only if you plan to keep the loan long enough to recover the cost. Paying points lowers the rate, but it also raises your upfront cost. If your credit is weak and your future is uncertain, locking extra cash into points is not always smart. I would only consider it after comparing the break-even time carefully.

Can a co-signer help me refinance?

Sometimes, but not always. Many refinance loans care more about the borrower’s own credit and ability to pay than a co-signer’s promises. A co-signer may help in some non-QM or special cases, but it is not the universal fix people hope it is. Ask the lender directly instead of assuming it will save the file.

So Where Does This Leave You

If your credit is bad, refinancing is not off the table. It is just less romantic than the internet pretends. You are looking for the loan that solves your actual problem, not the one that makes a clean headline or an impressive brag.

The best move today is simple: pull your mortgage statement, check your current loan type, and get a rough equity estimate. That tells you which doors even exist. Everything else comes after that.

And if the answer turns out to be “not yet,” that is still useful. It means you now know what to fix instead of guessing in the dark like everyone else.

Conclusion

You made it through the part most people quit on after three tabs and a headache. Respect. Refinancing with bad credit is not impossible, but it does punish sloppy thinking, and the mortgage world has never been shy about that.

The real trick is not chasing a miracle rate. It is choosing the least bad path that actually improves your life. That might be a streamline refinance, a wait-and-fix move, or deciding not to refinance yet because the numbers are nonsense. Sometimes the smartest financial decision is the one that looks boring from the outside. Funny how that keeps being true.