You’re staring at your mortgage statement, watching that equity number climb like it’s mocking your checking account. Of course it’s there years of payments, a hot housing market, and suddenly you’ve got $200,000 sitting in your walls doing nothing but making you wonder why life’s expenses always spike right then. We’ve all been there: the roof needs fixing, college tuition looms, or debt’s piling up faster than laundry in a house with kids.

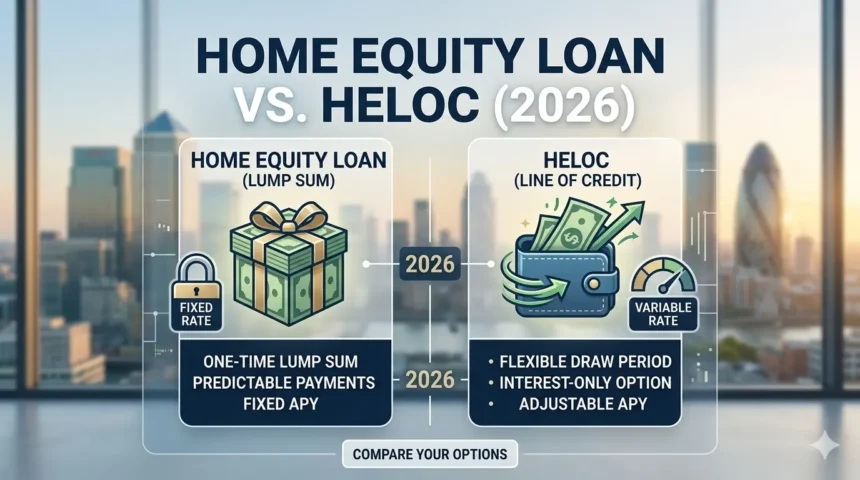

This isn’t some glossy bank ad promising easy money. Borrowing against your home’s equity sounds smart until you realize your house is collateral miss payments, and you’re not just late on a credit card; you’re risking the roof over your head. Home equity loans and HELOCs (home equity lines of credit) both tap that value, but one hands you a lump sum with fixed payments, the other acts like a credit card you can draw from as needed. Rates hover around 7.5% to 8% right now, lower than credit cards but higher than your original mortgage.

I’m not here to sell you on either. After helping folks navigate this for years, I know most regret rushing in without seeing the traps. Stick around we’ll cut through the jargon, compare them head-on, and get you to a decision that doesn’t bite later.

THE THING NOBODY ACTUALLY SAYS OUT LOUD

Your home’s equity isn’t “free money.” It’s a bet on your future self being smarter than your past self the one who maxed out the card on that impulse kitchen remodel. Banks love pushing these because your house secures it all, so they sleep easy while you sweat variable rates or balloon payments. Nobody tells you upfront: this can turn your biggest asset into your biggest liability overnight.

Think about it like that friend who co-signs a lease for you. Feels helpful until rent’s due and they’re calling the shots. With a home equity loan, you get cash now, fixed rate around 7.58%, repay over 10-30 years. Predictable, sure, but you’re locked in can’t adjust if rates drop further (they’re falling slowly in 2026). HELOC? More flexible: draw during a 5-10 year “draw period” at variable rates near 7.50%, pay mostly interest then. Sounds great for ongoing projects, like patching the roof now and adding solar later. But when the draw ends, repayments jump I’ve seen them double, turning “flexible” into panic.

Pop culture nails this: it’s the Home Alone trap looks fun until the iron hits your head. Homeowners have record equity, $300k+ average, but 43% of mortgaged homes are “equity-rich” now, down slightly. Yet most articles skip how lenders appraise lowballing your house value, shrinking your loan by 20%. You need 15-20% equity post-loan, credit over 680, DTI under 43%. Miss that, and you’re approved but for peanuts.

The dirty truth? These work for the steady engineers with pensions, not gig workers. I’ve watched freelancers celebrate HELOC approval, then freak when rates tick up 1% on prime index changes. It’s not evil; it’s math. But banks gloss the foreclosure risk: default, and you’re out. Real talk: if your job’s shaky or home values dip (they can), this isn’t a lifeline it’s a noose disguised as one.

And here’s the kicker nobody whispers: closing costs eat 2-5% upfront, $3k-$10k on a $200k loan. Roll them in? Higher balance, more interest forever. You’ve built equity to borrow it back at a premium. Hilarious, right? If you’re not obsessively tracking rates weekly, you’re playing roulette with your nest egg.

HOW THIS ACTUALLY WORKS THE REAL MECHANICS

Home equity borrowing exploded post-2008 when folks learned the hard way about over-leveraging. Today, with mortgage rates stuck high but equity loans dipping to 7-8%, it’s tempting again. Your equity? Home value minus what you owe. Zillow says average US home has $300k equity in 2026. Lenders cap at 80-85% loan-to-value (LTV), so on a $500k house with $200k mortgage, max borrow $150k-ish.

Home equity loan: apply, get appraised (costs $300-500), close like a mini-mortgage (2-6 weeks), lump sum hits your account. Fixed rate, say 7.91%, monthly principal + interest for 15 years. Like a second mortgage steady, but no take-backs.

HELOC flips it: approval gives a credit line, say $100k. Draw via checks/card during draw period (avg 10 years), pay interest-only (variable rate). Then repayment phase: 10-20 years, full principal + interest. Rates tie to prime (around 7.21% now). Flexible for serial fixers bathroom this year, deck next.

The niche banks ignore: appraisal roulette. Your $600k Zestimate? Lender appraiser says $550k to be “conservative.” Poof $50k less credit. Happens 30% of time in cooling markets.

Key mechanics, with my unfiltered take:

- Equity threshold (15-20% minimum): Banks want skin in game. Observation: immigrants/new buyers often short here build longer before tapping.

- Credit score (680+ ideal): Sub-700? Rates jump 1-2%. Real talk: fix errors first; one client boosted 50 points free via disputes.

- DTI under 43%: Includes new payment. Gig economy kills this lenders hate 1099s.

- Appraisal & closing (2-5% fees): $4k average. Skip no-fee lenders? They bake it into rate.

- Tax perk (maybe): Interest deductible if used for home improvements, up to $750k debt. But track receipts religiously IRS audits this.

- Rate types: Fixed loan vs variable HELOC. In 2026’s choppy Fed world, fixed feels safe but costs more upfront.

Daily life tie-in: You’re not Wall Street. This is funding braces or HVAC before it dies. But connect to reality rates fell from 9% peaks, yet still double credit cards. Mechanics matter because one wrong calc, and your “smart” move tanks retirement.

COMPARISON WHAT’S ACTUALLY DIFFERENT BETWEEN YOUR OPTIONS

| Option | What it actually does | Who it’s for | The catch |

| Home Equity Loan | Lump sum payout, fixed rate (avg 7.58%), fixed monthly payments over 5-30 years. | Folks needing one big chunk now like full roof replace or debt payoff. Steady income types. | Locked amount no flexibility if plans change. Higher closing costs 3-6%. Can’t borrow more later. |

| HELOC | Revolving credit line, draw as needed (up to 10 yrs), variable rate (avg 7.50%), interest-only then full repay. | Ongoing projects renos in phases, emergencies. Flexible budgeters. | Rates can spike (prime + margin), payment shock post-draw doubles bills. Temptation to overspend like a card. |

Skip the loan if you’re consolidating $50k debt HELOC lets you pay as you go. But for a $100k remodel? Loan’s predictability wins. My take: HELOC if rates stay low and you self-discipline; loan otherwise. Most mess up flexibility, so lean loan unless you’re disciplined.

WHAT ACTUALLY HAPPENS WHEN YOU TRY THIS

You call the bank, hyped on equity calcs. Appraiser shows your “upgraded” kitchen? They dock for “dated fixtures.” Line shrinks 15%. Surprise: they ignore your sweat equity. Closing drags three weeks, fees hit $5k on $150k loan. Funds wire, relief washes over.

First payment: loan’s $1,200/month fixed budgetable. HELOC? Draw $20k for furnace, pay $100 interest. Easy. Then rates nudge up 0.5% now $110. No biggie. But year 8, draw ends. Repayment kicks: $800/month jumps to $1,800. Pattern others miss: 80% underestimate phase shift. Clients call panicked, refinancing into worse fixed loans.

In practice, foreclosure whispers start at month 6 missed payments. Equity-rich? Sure, but underwater risk if values dip 10%. I’ve seen it 2022 buyers now equity-trapped. You try selling mid-HELOC? Buyers bolt from liens.

Concrete: My buddy Joe, 2024 HELOC for pool. Drew slow, fine. 2026 prime ticks, payments double. Sells house at loss to escape. What surprised me? Emotional toll guilt over “ruining” family asset. Most articles skip: this stresses marriages. Stats say home debt fights spike 25%. Real experience: pause 48 hours post-approval. Sleep on it. Too many don’t.

THE ADVICE EVERYONE GIVES VS WHAT ACTUALLY WORKS

“Shop rates!” Sure, but generic sites quote averages 7.5%. Your 720 score gets 7.2% at credit union, 8.5% big bank. Wrong because ignores personalized quotes. Works for: none universally. Alternative: Pre-qual 3-5 lenders online, no credit hit. My opinion: Credit unions crush banks 0.5-1% lower.

“Use for home improvements only.” IRS likes it for deductions, but life’s messy. Debt consolidation saves 10% vs cards. Incomplete for emergencies. Real alt: List three uses, cap at 50% equity. Stops abuse I’ve seen 100% taps lead to regret.

“HELOCs are free money during draw.” Interest-only lures overspenders. Misses balloon risk. Only works for cash-flow pros. Grounded: Model full repayment in spreadsheet first. Opinion: Avoid if DTI over 35%.

“Fixed rates always safer.” In 2026 drop? Locked at 7.9% while HELOCs hit 7%. Wrong for short-term. Alt: Hybrid loan for bulk, HELOC sliver. Direct: Rates falling? HELOC edges.

THE PRACTICAL PART WHAT TO ACTUALLY DO

Pull your latest mortgage statement and Zillow estimate. Calc equity: (home value x 0.8) – balance. Under $100k? Wait build more. Do this today; apps like Rocket Mortgage have free tools.

Shop three lenders: one bank (Chase), one credit union (Navy Federal), one online (Figure). Get pre-quals same week compare APRs, not just rates. Note fees; aim under 2%.

Run numbers in Excel: loan payment = PMT(rate/12, terms*12, amount). HELOC? Simulate rate +2%. If payment >5% income, stop. Free templates at Bankrate.

Order appraisal preview pay $100 for broker price opinion first. Avoids shocks. Local realtors do this cheap.

Check tax angle: Download IRS Pub 936. Log planned use (receipts). Non-home? No deduction pay cash instead.

Freeze non-essentials month post-approval. Builds buffer for shocks. Track via Mint app.

Talk spouse/kids unify on risk. Write “what if job loss” plan: side hustle list, 6-month fund goal.

SO WHERE DOES THIS LEAVE YOU

You’re armed now no more vague ads fooling you. Equity’s power, but house on line means treat like Vegas: bet what you replace. Not easy markets shift, jobs do. Rates low-ish at 7.5%, equity high, but risks real.

No perfection. Some thrive, others lose homes. Acknowledge: if DTI high or market wobbles, walk away.

Today: Calc your equity at Bankrate.com. Takes 2 minutes. If over $100k and DTI <35%, quote shop. Hold that number it’s your starting line.

Wait, You Read It All?

Props you outlasted most. Takes guts in a scroll world. Here’s the sticker: your home’s not a piggy bank; it’s your fallback. Choose wrong, regret forever; right, and you’re the hero. Messy as hell, but now you see it clear. Hit me if questions linger we both know banks won’t.